Okay so I'm SUPER behind on keeping you guys updated on our Total Money Makeover and apologize that I've completely dropped the ball on this.

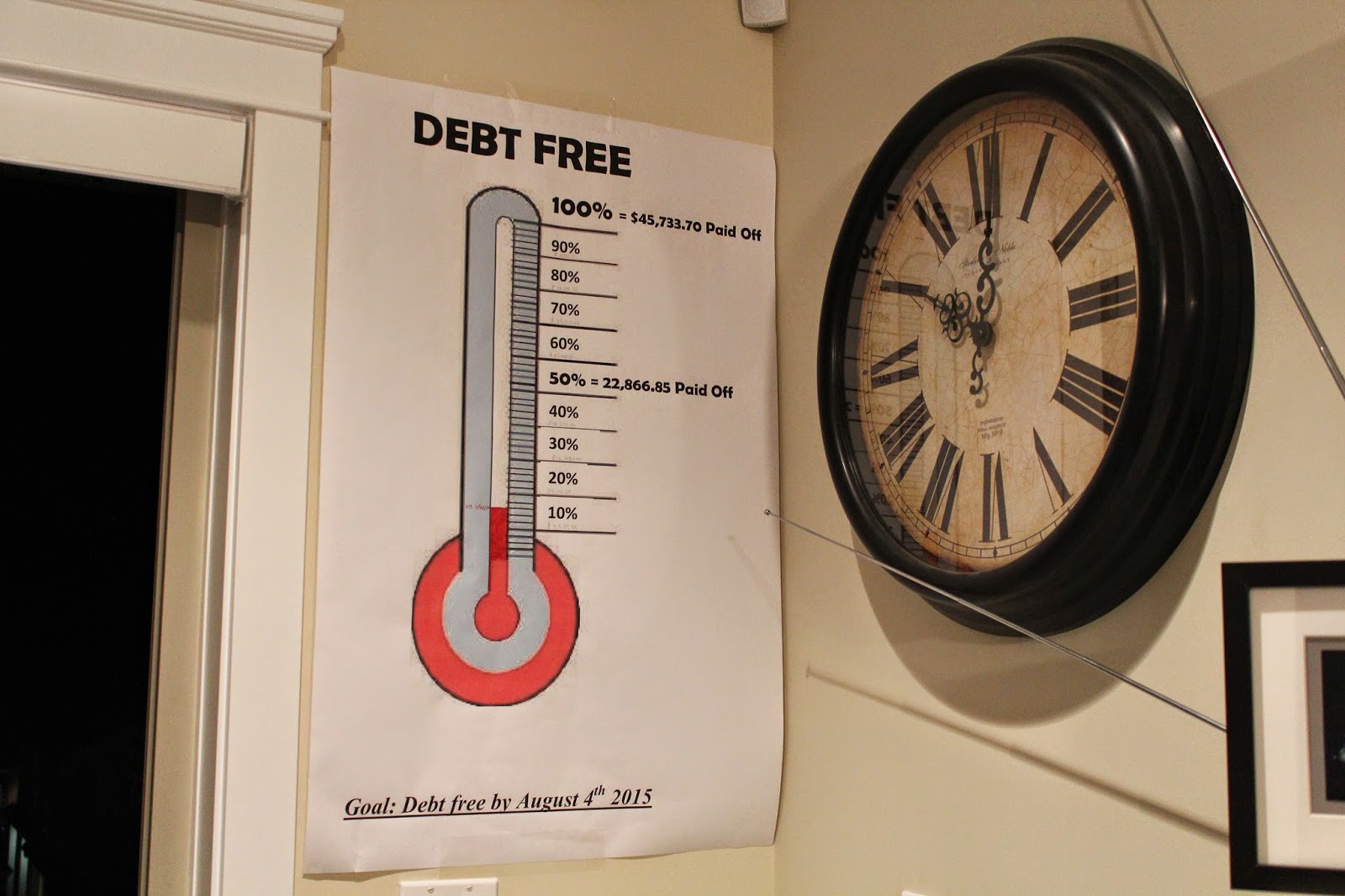

Here's a snapshot on where we're at with dumping debt.

***I wrote this back in April but never posted it. I've added even more of an update at the bottom***

Things have been a little rough financially since moving to New Jersey. Everything is so much more expensive....food, rent, auto insurance, and of course the fact that any time we want to go home we have to purchase tickets instead of just spending money on gas(yes we've been budgeting to pay for those flights but it's still an extra expense we didn't have before). AND we are paying out of pocket for Andrew to fly back to Oregon for all of his military obligations...a tough decision we had to make but feel good about what we decided (yes you may think we're crazy). Anyway, the first couple of months of living here we haven't had a whole lot of extra money to put towards debt.

BUT, on a good note we have been able to use cash envelopes which we weren't able to do in Canada. How cash envelopes work is at the beginning of the month or twice a month...however you want to do it, you get cash for different categories that are budgeted and place them in your envelope labeled with those categories. Then before you make a purchase you have to decide which envelope it comes from and use that cash to pay for the items. When the envelope is empty, no more spending till the next month when you fill it back up! For example groceries, we budget $285 for groceries (that amount was perfect back on the west coast but we've found that we may need to bump it up a bit now since things are not as cheap but we haven't done so just yet.). So, every time I go grocery shopping I take money from the grocery envelope and pay for the items...it's pretty simple. It really helps stay on track because you "feel it more" when you spend cash...you literally see the money going out rather than just swiping a card and looking at it later. It keeps you on track! Things like utilities don't have cash envelopes because we just pay them online with our debit card.

As for our debt, remember we paid off the Army Career Starter Loan in Oct. and only have Andrew's school loan left. During our move we were not paying more than just the minimum because we wanted to make sure we had extra money for the deposit on our rental and anything else that may come up. So to say it quite frankly, we have not been making any progress for several months now. It's disheartening because we haven't made any advancements toward our goal and August 4 will be here before we know it! Plus, here's another thing, remember how we were banking debt money in our savings when we were expecting Anneliese....well we're right back at that again. If you don't remember, the reason is because Dave Ramsey suggests to pile up a bunch of savings (extra money that would have originally been paid towards debt) when you are expecting a baby or a job loss. That way you have extra money to take care of things if need be. It really helped us last pregnancy because we had to pay the doctors out of pocket and then we got reimbursed from insurance a little bit later (that's how the Global plan worked, since we were living in Canada). With Anneliese's delivery, her and I were both healthy and we didn't need to use any of that money we had saved and so that was the big payment in October that bumped us over the halfway mark. SO, assuming this pregnancy and baby is just as healthy we will be able to put any money we've "banked" towards loans but no sooner than October.

I'm going to be honest, Andrew and I were bummed that even if we are able to save enough money to pay off loans (but it'd be sitting in savings for baby emergency) we wouldn't officially be debt free till past our goal of Aug 4. We started to think and discuss if we really actually needed to bank money or if we'd be okay without saving extra during this pregnancy. Then of course shortly after that discussion Andrew was listening to Dave Ramsey and a lady called in asking our exact question. Dave had a good point, he said "even if insurance covers 100% of bills, what if the baby had an emergency and needed to be flown to a specialty hospital....wouldn't it be nice to know you had extra money to be able to hop on an airplane without worrying about how to pay for that ticket, hotel and food?" That was a good enough explanation for Andrew and I, so we've started putting extra money in savings rather than towards our last debt. Besides, assuming we are blessed with a healthy delivery and baby, that money will go directly towards our debt anyway, it'll just in in October or November instead of August....not really a big deal is it? The answer is no...haha...but it still took us a little bit to get past the idea of not making our goal.

So that's where we're at. Still trying to figure things out with our budget here in New Jersey and banking any extra money we have for baby emergency.

Hope this all makes sense...I always feel like I try to cram so much information in one big breath on these posts. If you have any questions feel free to ask! =)

**Update** So I wrote this post back in April. At that time we were super bummed about not making our goal. However in April we received a large amount of money for "Tax Equalization"...meaning Andrews employer was making up for taking too much out of his paychecks when we were living in Canada since they weren't exactly sure how much to take out, with us living in a foreign country and all. Seeing that large amount in our savings (remember? our baby bank until Oct) has helped us to be okay with not making our goal and now we're trying really hard to add to it so that maybe we can just make ONE final payment...how awesome would that be?

And for those wondering, we only have about $20,000 of debt left!

And for those wondering, we only have about $20,000 of debt left!

|

| Taken from Dave Ramsey's Instagram |

.JPG)